How do I finance my acquisition?

Taking over a company requires a significant investment. Finding enough financing, especially for larger loans, is often a challenge. When financing is slow, postponement is not uncommon. A mix of financing forms — stacked financing — is often the best approach. That's according to Emmanuel Damman, head of business loans at PMV.

Discover more about acquisition financing on PMV's page.

As an entrepreneur, you need to assess how much you're willing to pay for a company and the timeframe within which you want to recoup that investment. "It's essential to get a clear picture of the value of the company you want to acquire," says Damman. "Hire an accountant or financial advisor. Examine the books to ensure the value is correctly estimated. This also strengthens your application for (additional) financing at PMV." The acquisition price is often expressed as a multiple of the EBITDA.

Mix of financing

Decide how you're going to finance the acquisition price. This is often a combination of personal funds and external financing. First, you should use your own liquid assets before approaching a bank for additional financing. Personal equity shows your financial commitment and belief in the project. However, not everyone has enough savings. Those who do may not want to invest everything in the purchase. “An acquirer is often expected to finance about a third of the acquisition price with personal funds,” Damman says. However, there are various ways to build personal equity, such as financial support from friends, family, or business angels. Subordinated finances are also seen by banks as ‘quasi’ equity. With sufficient (quasi) equity, you can obtain a traditional bank loan to cover the full acquisition cost.

Vendor loan

If you lack sufficient personal contribution, you can opt for a seller's credit or vendor loan. This is a popular way of deferring payment where the buyer pays part of the acquisition price later, as a loan. The annual M&A Vlerick study shows that this structure is being used more frequently. Let's say four managers want to acquire their company for 925,000 euros but can only raise 150,000 euros. Their share then represents only 16% of the asking price: too little for the bank. With a vendor loan of 150,000 euros, their equity increases to 300,000 euros, which is enough to borrow the remaining 625,000 euros from the bank. "A vendor loan raises equity cheaply and limits bank credit. The seller remains involved and receives a return: a win-win," says Damman.

PMV Solutions

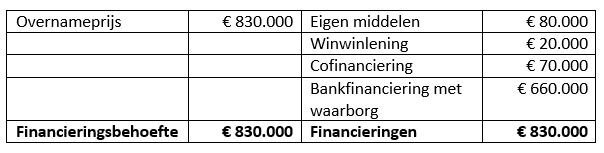

PMV/z offers various solutions that can be combined to generate sufficient bank financing: capital contribution, (subordinated) loan, or a guarantee. A guarantee provides the bank with more security when you cannot provide adequate guarantees. "A good financing mix is crucial to avoid debt repayment problems, especially in the first difficult years. An overly aggressive debt structure can lead to sleepless nights," Damman says. An example of a successful acquisition: a manager and his wife had only 80,000 euros as a personal contribution, but thanks to a well-thought-out business plan and various financing solutions from PMV/z, they managed to realize their dream.

Favorable financing

Damman continues: “The couple's parents each lent 10,000 euros through a Winwin loan over 8 years at 2% interest. This strengthened the equity. Besides the interest payment, the parents get an annual tax reduction of 2.5% on the loaned amount. In the event of a failed acquisition, they can reclaim 30% of the loan through a one-time tax reduction. The couple also relied on co-financing (70,000 euros) and a guarantee from PMV/z. As a result, the bank was willing to lend 660,000 euros with a government guarantee of 450,000 euros.

With all these financing solutions, the couple could gather enough funds despite their limited personal resources.

Read more on PMV's updated website.

Also interesting for you

Receive our newsletter

Leave your e-mail address and stay informed of our latest updates and offers. We will gladly keep you informed of new search results and relevant information.